Smartphone OLED panel shipments experienced a significant contraction in the first quarter of 2026. The total number of units shipped fell to 190 million, marking a 12 percent decline compared to the same period in 2025. This drop reflects broader industry challenges driven by a DRAM and memory crisis that has reduced overall smartphone demand.

Quarter-over-quarter decline reshapes competitive landscape

The quarterly decline was even more pronounced when compared to the previous quarter. Shipments decreased by 20 percent from the fourth quarter of 2025. This sharp downturn has reshaped the competitive landscape among major display manufacturers, altering market share distributions across the sector.

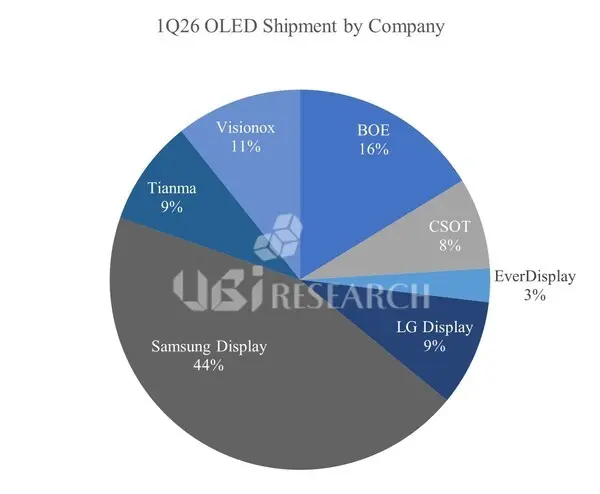

Samsung maintains its position as the dominant supplier with a 44 percent market share. Chinese manufacturer BOE holds the second-largest position at 16 percent, while LG accounts for 9 percent. LG has seen its reach increase by 1.4 percent compared to the first quarter of 2025, despite its smaller overall footprint.

BOE is gaining ground by offering lower prices, though it faces ongoing quality concerns. Based on Apple’s past experiences, the manufacturer still needs to resolve production problems. Samsung is rumored to adopt BOE’s technology for the base Galaxy S27 model to cut costs amid the memory shortage.

UBI Research and The Elec reported these market figures for the global, Chinese, and South Korean regions. The data highlights how supply chain constraints are influencing component sourcing strategies for major smartphone brands.

Discussion

0 comments

Log in to join the thread with a thoughtful take, question, or correction.